How liquidity metrics can make the difference when it comes to growth

This article is part 2 of the metrics mini-serie on financial metrics.

Companies want to expand their operations, grow into new markets, and serve new customers without compromising their profitability. To achieve this, you need to balance you cash in- and outflows by managing your liquidity. But how can you boost the financial health of your company to give it the best opportunity for growth?

Using metrics to measure your liquidity will help you to follow up your cash health and give you insights on how to improve it. Let’s take a look at some useful liquidity metrics and see the benefits they offer.

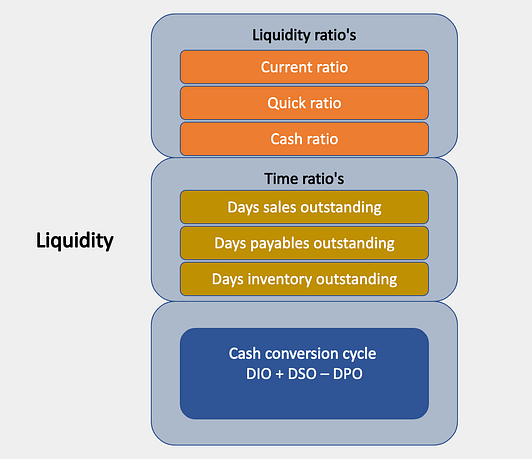

1. Current ratio

Also known as working capital ratio

Including all current assets and liabilities, the current ratio measures your company’s ability to pay short-term liabilities or obligations (within a year). It shows investors how your company can maximize your current assets to meet your current liabilities. It is worth noting that the current ratio only gives a snapshot into your finances, so doesn’t give a complete reflection of your short-term liquidity or longer-term solvency.

A current ratio in line with or slightly above the industry average is considered acceptable, while a lower ratio may indicate a higher risk of distress or default. However, if the current ratio is significantly higher than the industry average, it indicates that management might not be using its assets efficiently.

How to calculate your current ratio:

current assets / current liabilities

2. Quick ratio

Also known as the acid test

The quick ratio is an indicator of your company’s short-term liquidity position and measures your company’s ability to meet your short-term obligations with your most liquid assets, without selling stock or obtaining additional financing. The higher the ratio, the better the company’s liquidity and financial health.

As the quick ratio does not include inventory, which is difficult to turn into cash in the short term, it is considered more conservative than the current ratio.

How to calculate your quick ratio:

(current assets – inventory – prepaid expenses) / current liabilities

3. Cash ratio

The cash ratio tells creditors and analysts the value of your company’s current assets that can be quickly converted into cash and what percentage of your company’s current liabilities these cash and near-cash assets can cover. It is useful for creditors when deciding how much money they might be willing to lend to your company.

The results can be a cash ratio of 1 (the company has the same amount of current liabilities and cash), less than 1 (the company has insufficient cash to pay all current liabilities), or more than 1 (the company will have cash over after paying all current liabilities).

How to calculate your cash ratio:

(cash + cash equivalents) / short-term liabilities

4. Days sales outstanding (DSO)

Also known as days receivables or average collection period

How long does it take your company, on average, to collect payment for a sale? The answer is your DSO. Calculated on a monthly, quarterly, or annual basis, companies aim to receive payments quickly to keep their DSO as low as possible and ensure a smooth cashflow. Generally, a DSO of less than 45 days is considered low.

How to calculate your DSO:

(receivables/total sales) x days

5. Days payables outstanding (DPO)

As the opposite of DSO, DPO monitors the average time taken (in days) for your company to pay your suppliers, vendors, or financiers. Measured on a quarterly or annual basis, DPO indicates how well your company’s cash outflows are managed.

There are pros and cons to having a higher DPO. On one hand, it enables you to hold onto funds for longer so you can maximize benefits, increase your working capital, and free cash flow. But on the other hand, it can also be a red flag, indicating an inability to pay bills on time.

How to calculate your DPO:

(accounts payable x days) x cost of goods sold

6. Days inventory outstanding (DIO)

Also known as days days sales of inventory.

The DIO indicates the average time taken for your company to convert your inventory, including works in progress, into sales. In other words, it shows how long your company’s cash is tied up in inventory and how long the inventory will last. While the average DIO varies from industry to industry, a lower DIO is preferred as it indicates that it will take less time to clear inventory.

How to calculate your DIO:

(average stock / cost of goods sold) x 365

7. Cash conversion cycle (CCC)

CCC measures the time lag between the purchase of your company’s inventory and the receipt of cash from accounts receivable. By looking at how long your company’s cash remains tied up in your operations you can see how efficiently your managers manage your working capital.

A longer CCC means it will take longer to generate cash, which can mean insolvency for small businesses. A shorter CCC is a sign of a healthy company as it can use the extra cash to make additional purchases or pay off outstanding debts.

How to calculate your CCC:

DIO + DSO – DPO

days inventory outstanding + days sales outstanding – days payables outstanding

Talk to the experts

Interested in finding out more about liquidity metrics and how they can help boost your company’s financial health? Contact CFOrent for expert help and insights on improving your cashflows.

This is the first article in a four-part blog series on metrics in financial metrics. Click here to read part 1 on profitability, part 3 on net working capital and part 4 on solvability.