This article is part 4 of the metrics mini-serie on financial metrics.

What solvability tells your (potential) investors about your company

There are a lot of reasons for an investor to get involved in a particular project. He could like the company, be astounded by the product, or be impressed by the management team. However, underlying all these reasons is the investor’s desire to grow their investment. To achieve this, investors investigate opportunities from a variety of angles, with a particular focus on the company’s solvability metrics.

Unlike liquidity metrics that focus on the company’s capacity to pay short-term commitments, solvability metrics take a longer view by showing the company’s ability to meet its long-term financial obligations. By tracking solvability metrics, the company is in a better position to take strategic financial decisions based on valid information.

Good solvability can also convince investors about the benefits of investing in a particular company. For example, inflation has a knock-on effect, increasing interest rates which makes capital more expensive and leads to the contraction in the amount of available capital. When this happens, investors prefer to invest in companies with good solvability to ensure their returns instead of a high-risk, high-return option.

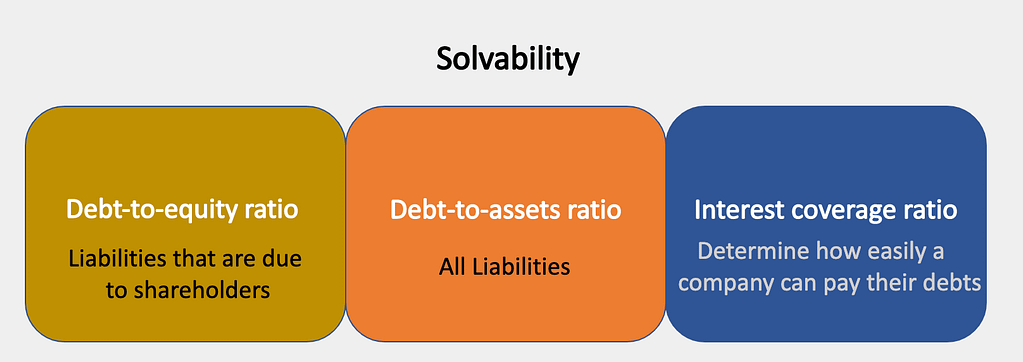

Let’s take a look at some solvability metrics and what they mean for your company.

- Debt-to-equity ratio (D/E ratio)

The debt-to-equity ratio is used to evaluate a company’s financial leverage, reflecting the capacity of shareholders’ equity to cover all outstanding liabilities in the event of a business downturn. Higher leverage ratios usually indicate a company or stock with a higher risk for shareholders and (potential) investors as it indicates that company is financing a large amount of its growth through borrowing.

How to calculate your D/E ratio:

total liabilities / total shareholders’ equity

- Debt-to-assets ratio (D/A ratio)

By considering all the company’s liabilities, such as loans, bonds payable, and all assets, including intangible assets, the debt-to-asset ratio indicates the company’s financial stability. The higher the ratio, the higher the degree of leverage, which means the higher the risk of investing in the company.

To give an example, if a company has a ratio of 0.4, then 40% of its assets are financed by creditors and the other 60% by equity. This is a useful metric to see how much debt the company already has and whether the company can repay its existing debts.

How to calculate your D/E ratio:

total liabilities / total assets

- Interest coverage ratio (IC ratio)

The interest coverage ratio is used to determine how easily a company can pay the interest on its outstanding debt as being able to pay interest payments is a critical and ongoing concern for any business. Once a company struggles to meet its obligations, it may be forced to borrow further or draw on its cash reserve, which would be better used to invest in capital assets or for emergencies.

The IC ratio is often used by lenders, investors, and creditors to determine the risk of a company based on its current debt or for future loans or investments. Generally, a higher ratio is better.

How to calculate your D/E ratio:

earnings before interest and taxes (EBIT) / interest expense

Talk to the experts

It’s important to remember that it costs money to borrow capital, whether that’s in the form of investment or loans. The costs of this capital could be interest payments, in-kind agreements, strategic concessions, or a liability in another form. Contact CFOrent to ensure reliable calculation of your solvability ratios to generate the capital your company needs to grow.

Contact us for more information.

This is the first article in a four-part blog series on metrics in financial metrics. Click here to read part 1 on Profitability, part 2 on liquidity and part 3 on net working capital.